How a 3(38) fiduciary can help you manage your retirement plan

You’ve decided you want to offer your team a 401(k), but now you’re worried about the responsibility that comes with it. It can feel scary to offer a 401(k) because it’s a federally-regulated benefit, and you’re making a decision that could impact your business and your employees.

As a 401(k) plan sponsor, one of your duties is to monitor the appropriateness of investment options under the plan. This may include options that are actively managed. Plan sponsors have to decide who will handle the investment management responsibility of their plan’s investment offerings. This person or group is known as a fiduciary. A plan sponsor could serve as the fiduciary or outsource it to a third-party provider.

Guideline acts as a 3(38) investment fiduciary, which means we can make investment decisions on behalf of our customers. We’ll break down what this means below, as well as:

- What is a fiduciary?

- What is the role of a fiduciary?

- What are the different kinds of fiduciaries?

- What should you consider when choosing a fiduciary?

Let’s get started.

What is a fiduciary?

When it comes to a 401(k), a fiduciary is a person or group who must act in the best interest of all of the plan’s participants

Some fiduciaries — such as an employer, a company officer, or a third party — are listed by name in the plan document. Other fiduciaries aren’t necessarily listed by name, but upon appointment by another plan fiduciary. A person or entity is a fiduciary if they make decisions about the plan's assets.

What are the different kinds of fiduciaries and how do they differ?

There are three types of fiduciary roles identified under Section 3 of ERISA:

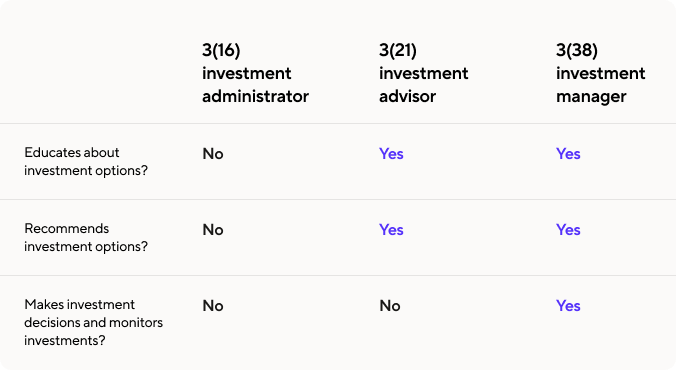

- 3(16): The fiduciary has an administrative role, including meeting ERISA requirements for reporting, making disclosures, and filing the correct paperwork.

- 3(21): The fiduciary can make investment recommendations to another fiduciary.

- 3(38): The fiduciary can make investment decisions on the client’s behalf. In general, a 3(38) fiduciary must be a registered investment advisor (RIA) under federal or state law, an insurance company, or a bank.

Guideline is registered with the Securities and Exchange Commission (SEC) and acts as a 3(38) fiduciary for all of our plans. We are responsible for managing our plans’ investment portfolios and selecting and monitoring funds.

Note: while we offer 3(16) fiduciary services, they are only available to clients who use an eligible payroll provider.

Now, let’s take a deeper dive into 3(38).

What is a 3(38) and what are they responsible for?

Under a 3(38) investment management agreement, we’re responsible for selecting and monitoring funds, as well as managing investment portfolios for our customers' plans. This can include replacing funds and updating model portfolios as needed.

3(38) fiduciaries have strict standards of conduct, responsibility, and obligations. Under the Employee Retirement Income Security Act of 1974, or ERISA, some of the main requirements are to:

- Act responsibly and in the best interest of the plan and its participants

- Determine that the plan’s investment options are appropriate and that there are enough options to allow participants to diversify and help minimize the risk of large losses

- Follow the plan’s document

- Avoid conflicts of interest

What is the difference between 3(21) and 3(38) fiduciary?

3(21) fiduciaries typically only provide advice regarding investment to another fiduciary. They generally don't manage funds.

What are the benefits of a 3(38) fiduciary?

A 3(38) fiduciary assumes most of the risks and responsibilities associated with offering investments under an employer-sponsored retirement plan. They’re in charge of the investment portfolio and selecting and managing funds.

Even if you’ve appointed a third-party as an investment fiduciary, you’re still ultimately responsible for your plan. That’s why as a plan sponsor, you need to ensure that the fiduciary you appoint is an appropriate choice. The good news is you can confidently delegate a lot of the investment responsibility by choosing a 3(38) fiduciary who will be committed to acting prudently when making investment decisions on your behalf. By working with a 3(38) like Guideline, you can help limit your investment responsibility. You’ll get the peace of mind that your employees’ retirement plan is being managed by investment professionals.

What are Guideline’s guiding principles as a 3(38)?

Guideline acts as a 3(38) investment management fiduciary on all of our plans. Our fiduciary duty legally requires us to act in the best interest of all of our plan participants.

Our investment committee regularly reviews investment strategies and performance. Our simple and time-tested investment philosophy is focused on minimizing fees, diversifying broadly, and playing the long game. Our software, customer service, and industry experience help us meet these expectations.

Our ultimate mission is to help everyone arrive at a secure retirement. In addition to our low-cost funds, our asset-based fees are up to 10 times lower¹ than the industry average. While a few tenths of a percentage point may not seem like it would make a difference, when looking at long-term growth over the course of an individual’s retirement savings journey, it can really add up.

We realize it’s unrealistic for all plan sponsors to be investment experts. Offering a Guideline 401(k) can make the experience of administering a 401(k) easy and affordable. Put simply, this allows business owners and benefits managers to focus on what matters most — keeping employees happy and growing your business.

This information is provided for illustrative purposes only, and is not intended to be construed as investment or tax advice. We recommend that you consult a qualified tax and financial advisor to determine the appropriate investment strategy for you. Guideline makes no guarantees with regard to investment performance, as investing involves risk and your investments may lose value.

¹ The average investment expense of plan assets for 401(k) plans with 25 participants and $250,000 in assets is 1.60% of assets, according to the 23rd Edition of the 401k Averages Book, with data updated through September 30, 2022,, and is inclusive of investment management fees, fund expense ratios, 12b-1 fees, sub-transfer agent fees, contract charges, wrap and advisor fees or any other asset based charges. Guideline’s managed portfolios have blended expense ratios ranging from 0.064% to 0.07% of assets under management. When combined with an assumed 0.08% account fee, (Alternative account fee pricing is available, ranging for .08% to .035%), the estimated total AUM fees for one of Guideline’s managed portfolios can be under 0.15%. Expense ratios for custom portfolios will vary. These expense ratios are subject to change by and paid to the fund(s). View full fund lineup here. See our Form ADV 2A Brochure for more information regarding fees.