Exposing the small business 401(k) access gap

Since day one of building Guideline, we’ve known that small businesses have historically been at a disadvantage when it comes to offering their employees a retirement plan.

From our perspective, it’s no mystery why. Legacy 401(k) providers avoid small businesses because they’re too difficult for them to turn a profit on. Instead they either refuse to take on new clients under a certain size or charge them prohibitively high fees. The result? Small and mid-sized businesses are left in the cold without an easy way to offer meaningful retirement benefits. Which is why we set out to build a more modern and affordable approach to retirement planning that works for businesses of every size.

But despite the obvious gap in access, defining just how big it is has proved to be challenging. Some reports say half of small business employees in the private sector don’t have access to a retirement plan, but what is the definition of a “small business” in terms of employee count? It turns out, putting some numbers behind this topic is easy when you approach it from a data standpoint.

For those who are unaware, and it may be most of you, if you are a business that offers your employees a 401(k), you are required by law to submit a Form 5500 every year, which provides some details about the plan you offer. These forms are then made public. And it turns out, if you pool many of them together—say 500,000 of them—the result is a treasure trove of compelling data that paints a pretty clear picture of the 401(k) market in the United States today.

Our data team analyzed more than 500,000 submitted forms to pull insights about how many small businesses offer their employees a retirement plan, and what participation looks like at those that do. I’m excited to break down what we discovered.

Number of small businesses in the U.S.

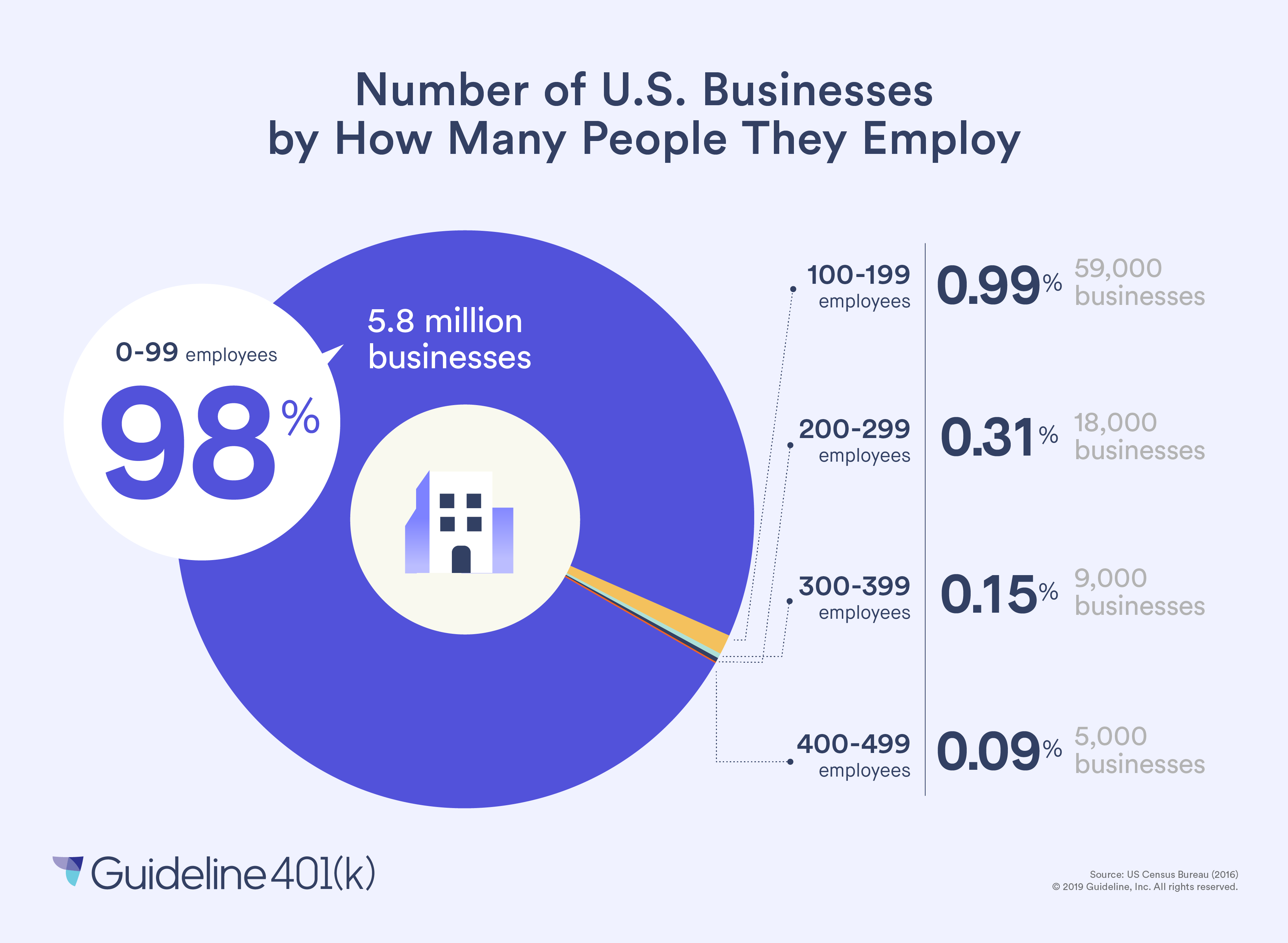

We first set out to determine just how many small businesses there are. The US Census Bureau provides very helpful information regarding how many businesses there are divided clearly by employee count. For the sake of definition, we’ve considered a small business to be one that employs between 0-99 people and have looked at businesses that employ up to 500. The below research is based on those two considerations.

There are more than 5.8 million small businesses in this country. That number decreases dramatically the higher the employee count climbs—there are approximately 59,000 businesses that employ between 100-199 people and about 18,000 that employ 200-299 people, and so on. We’ve included a full breakdown above.

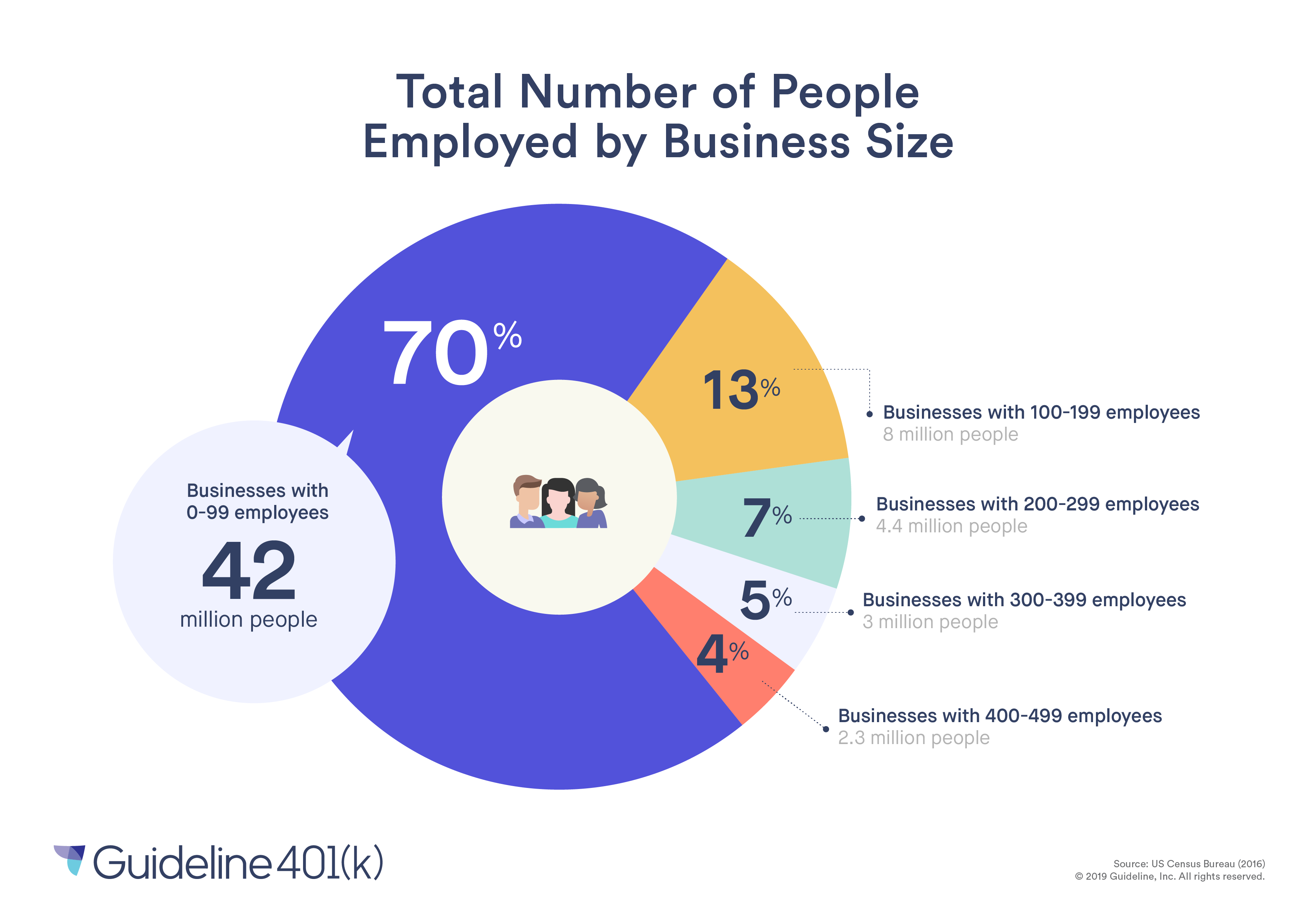

Let’s dive deeper. How many individual hard working Americans work at a small business? More than 42 million. That means more than 70 percent of working Americans—who work at businesses that employ 499 people or less—work at a small business. So regardless of whether we look at the number of businesses (5.8 million) or number of workers (42 million), the small business sector as defined by 99 or fewer employees is a big sector of the US economy.

What percentage of small businesses offer a 401(k) plan?

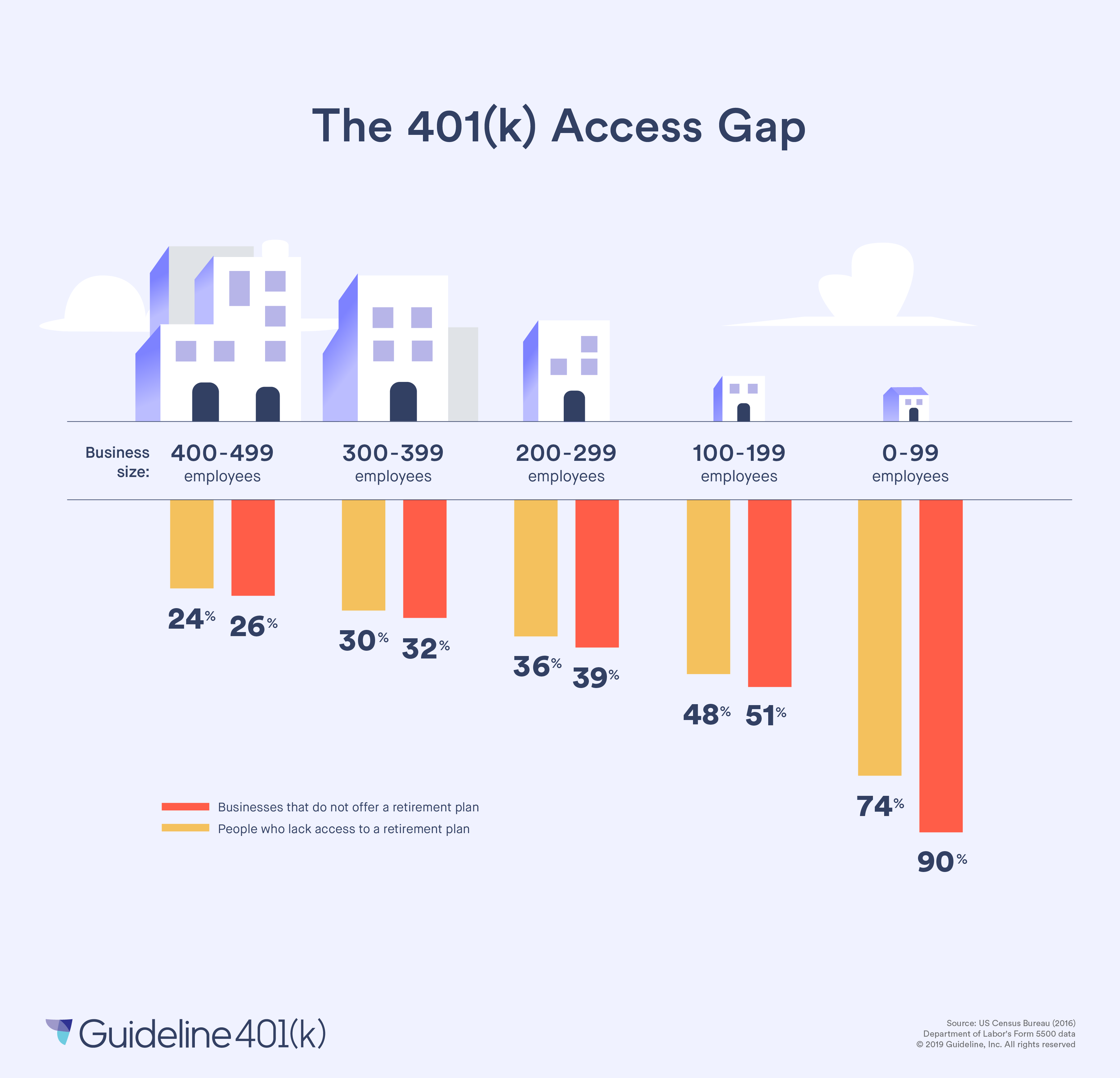

Now that we’ve outlined just how large the small business community is, let’s get back to the task at hand: determining how many of them offer their employees an employer-sponsored retirement plan. I’m afraid things are about to get bleak. According to our research, of those 5.8 million small businesses, 90 percent of them do not offer their employees a 401(k); of those 42 million people who work at a small business, 75 percent of them do not have access to a retirement plan.

The access gap is more narrow for folks who work at larger businesses, but it still isn’t great. Above is a visual breakdown of what percentage of businesses offer their employees a retirement plan depending on how many people they employ. For additional perspective, we’ve also included a breakdown of what percentage of workers have access by employee size grouping.

Not all the numbers are negative. Even though 75 percent of small business workers lack access to a 401(k), of those who are offered one, 70 percent of them participate. That number is a bit higher when looking at just Guideline plans—our participation rate is 83 percent. A high participation rate is a very important point amidst this data because it shows this is a benefit this cohort of workers actually wants, despite how few of them are given the opportunity.

Guideline

While this data adds to the growing evidence of a serious retirement crisis in this country, for us at Guideline, it reaffirms the importance of our mission: to create a retirement people can look forward to. There are over 25,000 businesses offering their employees a Guideline 401(k) plan, and we’re proud that 99% of them are small businesses. I’m sure at this point you know that isn’t a coincidence.

The days of alienating small businesses from modern and affordable retirement planning are over. Building something catered to the needs of 98% of American businesses that employ between 0-499 people is not just a very compelling business opportunity, it’s also the right thing to do.

So back to work we go.

P.S. If you find crunching insights and numbers to find compelling business opportunities as exciting as we do, we’re hiring in data science and data engineering at our offices in Austin and San Mateo. Join us.

Methodology

We leveraged the U.S. Census Bureau's 2016 Statistics of U.S. Businesses (SUSB) annual datasets to understand the number of businesses and workers. The number of retirement plans and employees accessible to plans was pulled from Department of Labor's Form 5500 data sets. We also analyzed employer sponsored Guideline 401(k) plans as of March 23, 2019.