Your 401(k) is garbage…but it doesn’t have to be

Over the last few weeks, I have been reading about the investment industry enriching themselves with outsized fees from retirement plans for teachers. This follows a wave of lawsuits against several major universities, including Duke, Johns Hopkins, MIT, NYU, Penn, Vanderbilt, and Yale for high fees and mismanagement of their faculty and staff retirement plans.

It doesn’t have to be this way.

I am thrilled to be joining Guideline as the Chief Operating Officer to help build the modern retirement plan that today’s workforce deserves. We are starting with a laser focus on serving small businesses, for which there are essentially no existing 401(k) offerings today.

My journey to Guideline began in 2010, when I joined a startup called kaChing in an old drive-thru dry cleaner in Palo Alto. kaChing pivoted to become Wealthfront, where we pioneered the new “robo-advisor” market, bringing individual investors transparent, diversified, low-cost, rebalanced, and tax-optimized portfolios. We also developed rich, interactive content to help educate our clients about their financial decisions.

The overall effect of the development of the “robo-advisor” market has been to encourage more Americans to invest, and to do so in higher quality and lower cost portfolios. It has also put pricing pressure on traditional advisors, who historically have charged 1% or more on their clients’ assets.

During my time at Wealthfront, I met with a steady stream of tech companies to talk about how we could help their employees sell their stock to further their personal goals like paying down debt, establishing an emergency fund, buying a home, and investing towards their kids’ college education and their retirement.

In those discussions, the company execs would inevitably ask me where they could find a simple, transparent, and low-cost retirement plan for their employees. I never had a good answer for them, which was frustrating.

Enter Guideline

Fast forward to early 2015, when I was introduced to Kevin Busque, the cofounder of TaskRabbit. Kevin had recently left TaskRabbit to start a new company to disrupt the retirement plan market. He was authentic and passionate about the opportunity because it grew out of his frustration to find a great 401(k) for the TaskRabbit team.

Kevin and I chatted regularly, and it began to dawn on me how broken the U.S. retirement system had become, with the dismantling of corporate pension plans, the egregious and opaque fees charged by the investment industry, and shifting demography leading to more years in retirement.

We have reached a point where the typical American worker doesn’t have nearly enough to retire, let alone cover minor emergencies. There are three main aspects to this problem — limited access, low participation, and lousy investment options.

Limited access

Almost half of all working Americans lack access to a retirement plan through their employer. This is significant because employer-sponsored plans are still the best way to save for retirement. They have high contribution limits, enable pre-tax contributions, and many employers offer a matching contribution, which is free money to the employee.

But the employer-sponsored retirement system has largely ignored small business employees. In California, for example, 7.5M small business employees don’t have access to a retirement plan through their employer!

Low participation

Unfortunately, many eligible employees at employers of varying size choose not to participate in their company retirement plans. Among those that do participate, most don’t contribute nearly enough to build a sufficient nest egg to maintain their lifestyle when they reach retirement.

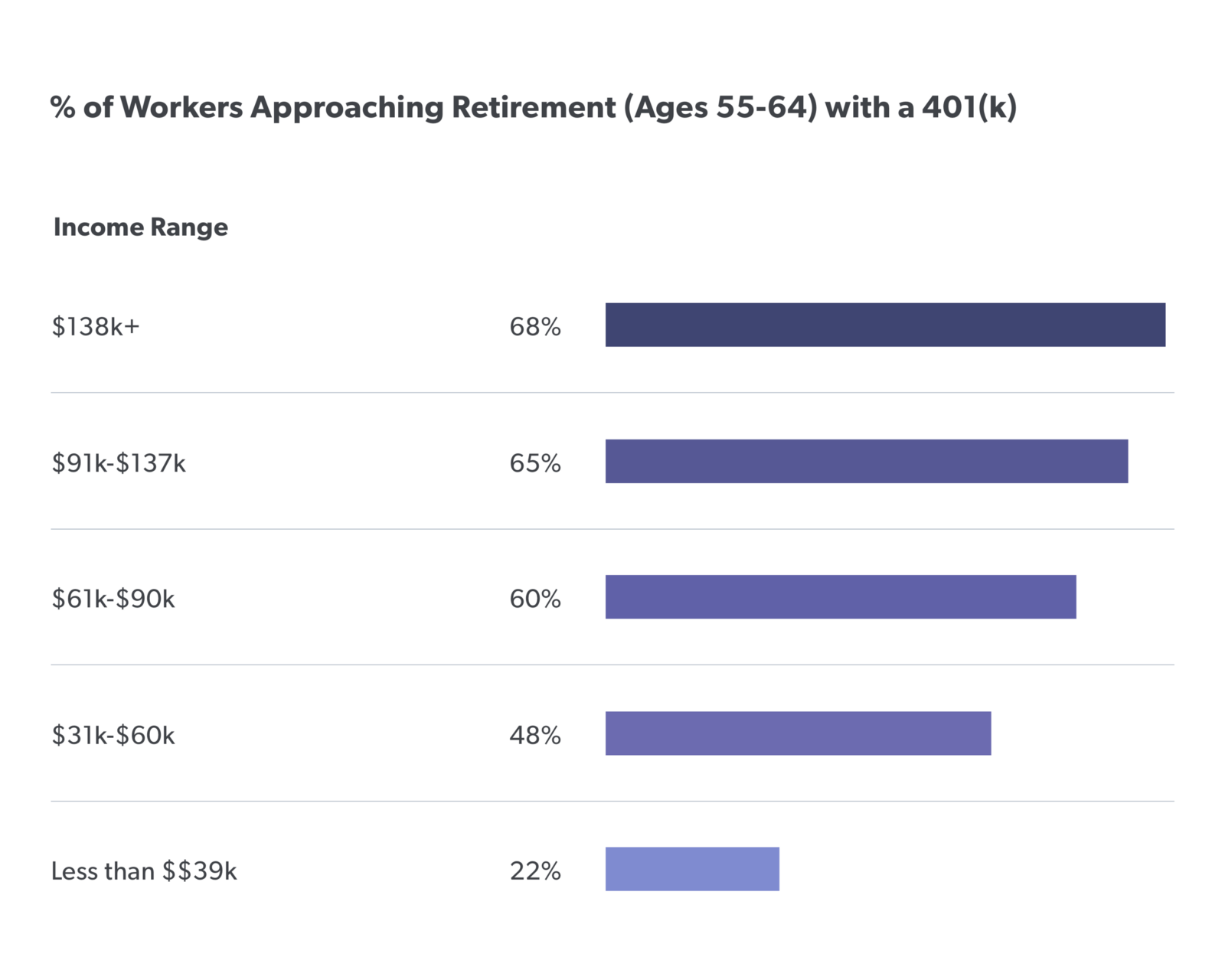

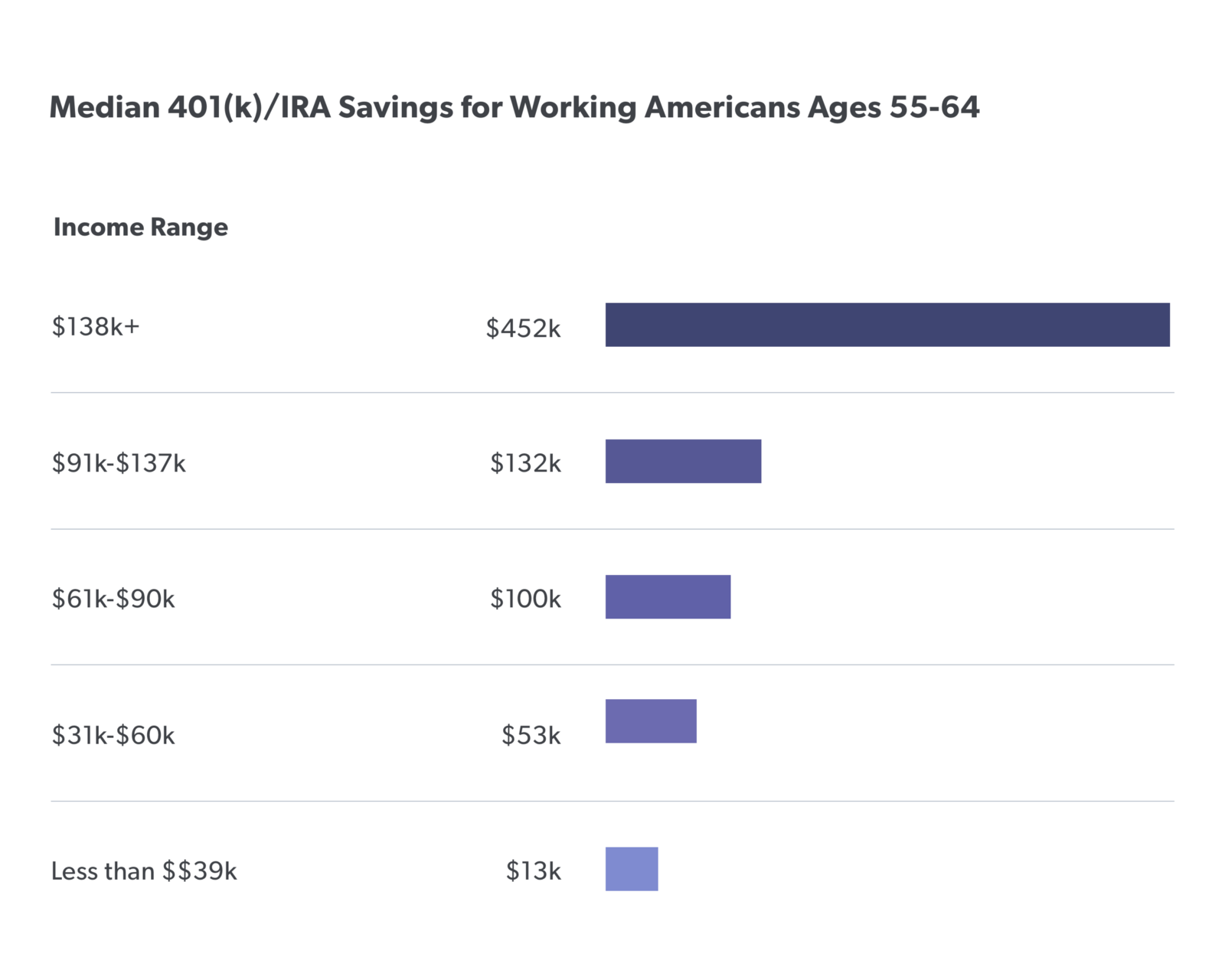

The typical worker approaching retirement (i.e. aged 55–64) has only $111,000 in total retirement savings in their 401(k) and IRAs. This translates to less than $400 per month in income during their retirement years (source: Falling Short by Ellis, Munnell & Eschtruth).

Several economists have studied the participation problem and found that making retirement plans opt-out through auto-enrollment, rather than opt-in, can double participation. And starting the default contribution at 3–4% of an employee’s salary and gradually increasing it over time can make a significant impact on the amount they have when they reach retirement.

Lousy investment options

For the employees with access and who contribute, what awaits them inside their plan isn’t pretty. Most retirement plans have a bewildering array of investment options, making it difficult for participants to make good choices.

They also have layers of opaque fees buried in the fine print, and many use mutual funds with unnecessarily high fees. If the multi-billion dollar retirement plans from many of the country’s elite universities have these issues, you can imagine how ugly it gets for much smaller plans.

Big problem = Big opportunity

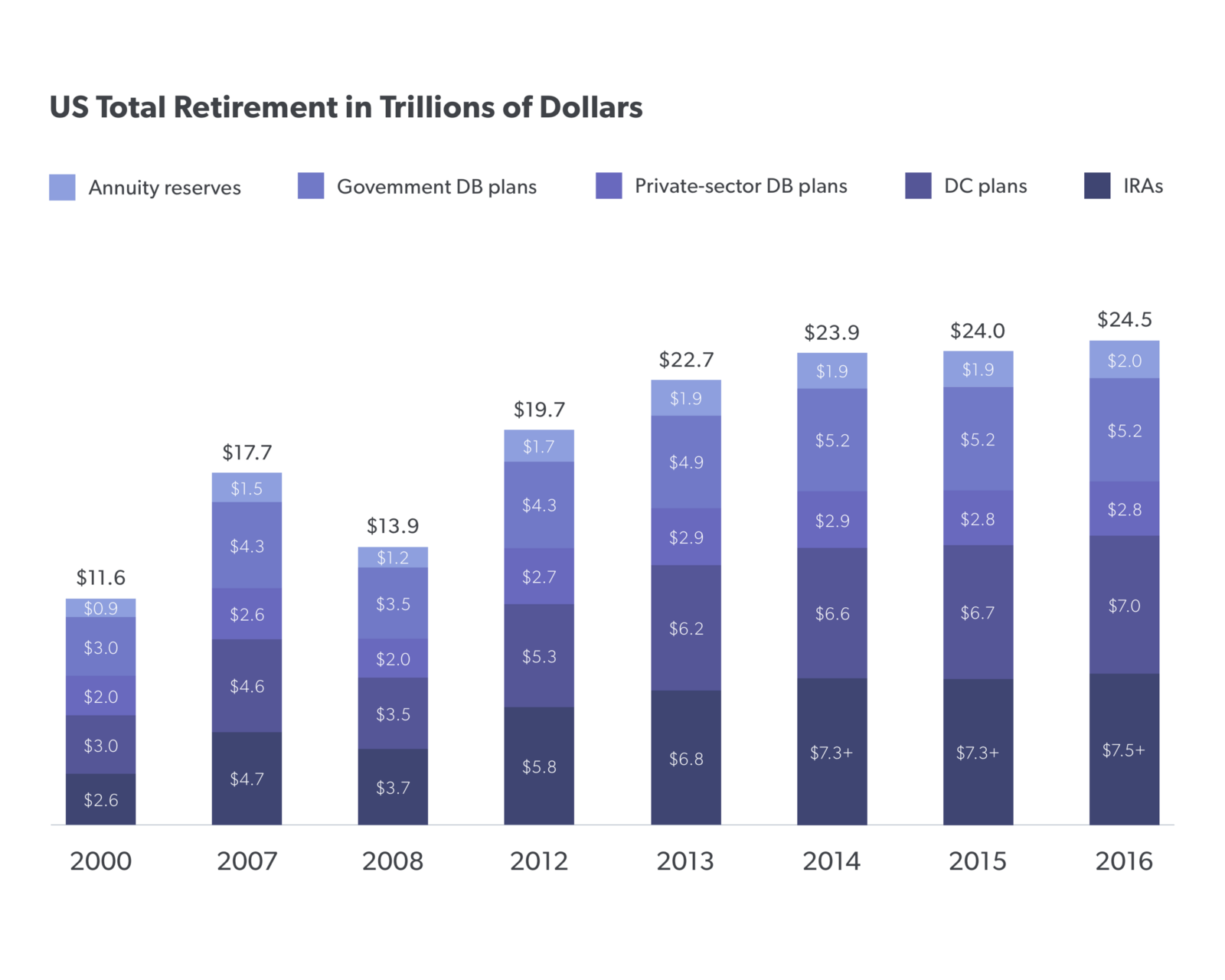

The dysfunctional U.S. retirement system creates a staggeringly large opportunity. While there is almost $25 trillion in total retirement assets today, much of it is mismanaged, and it isn’t nearly enough money to meet the needs of future retirees.

The retirement plan market is set to grow from here, as small businesses come online with new plans. Nearly half of the private sector U.S. workforce is employed by small businesses, and several states are mandating access to workplace retirement plans.

Just a few weeks ago, Governor Jerry Brown signed the new Secure Choice law requiring California small businesses to offer a workplace plan to their employees or use a new state-developed plan.

Why Guideline is different

Guideline is a full-stack startup uniquely positioned to disrupt the retirement plan market. The cofounders started out by building a record-keeping platform, and then we added plan administration, investment management, and compliance.

The only third parties we use are our custodian, who plugs into State Street, and Vanguard, for their low-cost funds. This allows us to minimize our fees for employers (plan sponsors) and their employees who use our service.

Our modern 401(k) starts at $8 per employee per month, plus a $39 monthly base fee. Employees don’t pay any fees to our custodian and they pay an average of 0.06% for the index funds in our managed portfolios (i.e $6 for every $10,000 invested).

This model, not dissimilar from how software company Slack prices its service, allows us to focus on engagement and participation. We think this creates the best alignment with our clients — employers and employees.

Why now?

Retirement plans remain one of the few areas of the financial markets largely untouched by the internet. We are going to change that.

Regulatory change, including Secure Choice in California, growing awareness about the importance of transparency and low investment fees, and today’s workers expecting a delightful user experience, will help galvanize the development of this new market for small business plans.

The traditional retirement plan providers, Fidelity being the gorilla, are likely to remain ambivalent about small plans because they are uneconomic to them, given their distribution model and focus on % asset management fees.

I am delighted to be joining Guideline because we are well positioned to build a great technology company to focus on the needs of the employer and employee. We are dedicated to bringing a 401(k) plan to market that remedies the issues with limited access, low participation, and sub-par investment plan options. Join us.