How to choose a small business 401(k) provider

The global economy is having a big impact on small businesses across the country. To help small business owners and their employees stay informed during this challenging time, we’ve gathered information on 401(k) savings, investing, and more. For the latest news and insights, visit our resource hub.

Whether you’re shopping for a car or just lunch, you’ll probably do your due diligence beforehand. Choosing a small business 401(k) provider shouldn’t be any different.

The race for talent, coupled with the fact over 90 percent of employees expect retirement benefits, has created a crowded market of 401(k) providers, consultants, and technology platforms. But nearly a quarter of small business owners admit they’re “flying blind” when it comes to selecting a 401(k) solution.

When you make the right choice, you’ll know it—employees are engaged, costs are low, and administration is easy. When you don’t, it can be a costly mistake and compliance liability. Here’s what to consider when choosing a 401(k) provider.

Table of contents:

- Decide how involved you want to be

- Know your fees

- Ask about plan features and options

- Prioritize user experience

- Ask about payroll integrations

1. Decide how involved you want to be.

✅ Guideline handles administration, compliance, and investment management for one low fee. Learn more >

No matter how seamless the front-end experience seems for employees, offering retirement benefits involves a lot of behind-the-scenes work. Sure, there are plenty of upfront challenges, like finalizing your plan design and deciding whether you’ll offer both traditional and Roth 401(k) contributions. But the biggest time commitment might involve day-to-day maintenance, compliance, and reporting. Below are just a few of the core duties handled by a 401(k) plan administrator.

- Preparation of Summary Plan Description for participants and beneficiaries

- Participant disclosure documents and account statements

- Approval of transactions (e.g., loans, distributions)

- Compliance with plan rules and federal laws

- Discrimination testing and audit support

- Employee enrollment and communications

- Required Internal Revenue Service and Department of Labor filings (e.g., Form 5500)

If that sounds like a full-time job, that’s because it is (we’re hiring!). Small businesses often turn to third-party administrators (TPAs) to handle these responsibilities on their behalf. Even TPAs vary widely in their scope, responsibilities, and accountability. For example, ERISA 3(16) fiduciaries take on administration duties and liability for ensuring your plan is compliant with the Employee Retirement Income Security Act (ERISA).

If that wasn’t daunting enough, remember that there’s more to managing a retirement plan than administration and compliance. Unless you want to handle your plan’s investment strategy yourself, you need an investment advisor and manager.

2. Know your total expense ratio.

If you’re looking for a metric that sums up how much your 401(k) plan might cost employees, look no further than your total expense ratio. This is simply the percentage that participants are charged based on their holdings. For example, a 1% expense ratio means that an employee with $100,000 in their 401(k) account would be charged $1,000 per year. As you evaluate providers, ask about their average expense ratios and other fees.

So what’s considered a fair market expense ratio? It depends on your size. While it sounds counterintuitive, smaller companies usually have higher expense ratios. Businesses with 50 employees have an average expense ratio of 1.68%. In comparison, the average ratio for a company with 2,000 employees is 0.7%. While those percentages sound small, they result in exponentially higher fees as holdings grow. Because small businesses have enough to worry about, Guideline keeps its average expense ratio for managed portfolios down to just 0.067%.

3. Ask about plan features and options.

✅ Guideline offers a full suite of options for companies and their employees, including traditional, Roth, and Safe Harbor plan designs. Learn more >

There’s no one-size-fits-all approach to saving for retirement. Employers have access to a variety of creative solutions for boosting participation and rewarding employees who save. You’ll want to make sure that the providers you consider can accommodate your needs.

One of the first things you’ll want to confirm is whether the provider supports both traditional and Roth 401(k) contributions. The difference between the two has to do with when the dollars are taxed. Employees with traditional 401(k) accounts make their retirement contributions before taxes and these amounts grow tax free until they start withdrawing funds. The thought is that tax brackets will be lower after retirement. Conversely, those with Roth 401(k) accounts make their contributions after-tax. These amounts grow tax free and are tax free to employees at distribution so long as they are held for at least five years. Though Roth contributions take a bigger bite out of employee paychecks, the arrangement is popular with younger workers since they have a longer runway to retirement. Choice is king—bottom line, any reputable vendor should support both types of contributions.

Safe Harbor 401(k) plans are also worth considering. These special plans are exempt from certain compliance obligations but, in turn, require you to contribute to your employee’s 401(k) accounts. Given that both employer matching and profit-sharing are two great ways to boost participation, retain talent, and even save on taxes, the arrangement might be a no-brainer for your company. Just make sure that the 401(k) plan providers you’re evaluating can actually accommodate Safe Harbor plans and matching arrangements.

4. Prioritize user experience

✅ Guideline makes it easy for employees to check their balances, contribution rates, and more — all in one place.

Managing retirement benefits should be easy for both your business and its employees. As you consider your options, pay careful attention to user experience. Does the provider’s technology make it easy for participants to roll over a previous retirement account? Does it give employees access to a single dashboard where they can check their balance, view transaction data, update contributions, and check in on your employer match? The harder this information is to find, the less perceived value employees get from your retirement offering. Additionally, consider whether the provider has a mobile app or is mobile enabled, so that employees can securely access their account information on the go.

As intuitive as the software might be, it’s a safe bet that employees will have retirement-related questions along the way. Your small business’s HR team (if you even have one) is already wearing a lot of hats — don’t force them to add “retirement expert” to the list. You may want to work with providers that bundle their software with service catering to all of your users, including HR professionals and 401(k) participants.

5. Ask about payroll integrations

✅ Guideline integrates with leading HR and payroll providers, eliminating the administrative hassle of processing and updating 401(k) contributions.

Payroll and retirement go hand in hand. When employees update their contributions, they trust those amounts will be deposited into their retirement accounts after payday. In the past, making that happen required HR to manually enter deferrals into payroll. That approach is time-consuming and prone to administrative errors.

When considering 401(k) providers, weigh whether they have a full 360 integration with your HR and payroll software. There are benefits beyond streamlined contributions, too. If you want to auto-enroll new hires into a 401(k) account, ask whether the providers’ integrations support that. Investing in a solution that keeps HR, payroll, and retirement in sync not only saves time and money, but makes for a better employee experience overall.

Guideline fully integrates with providers such as Gusto, Zenefits, Rippling, and ADP. Do you outsource payroll to a professional employer organization? No problem. We work with PEOs like Justworks.

Evaluating 401(k) providers can be intimidating, which is why small businesses often put off the decision. But delaying further can put companies at a competitive disadvantage, as jobseekers increasingly see employer-sponsored retirement benefits as a must-have.

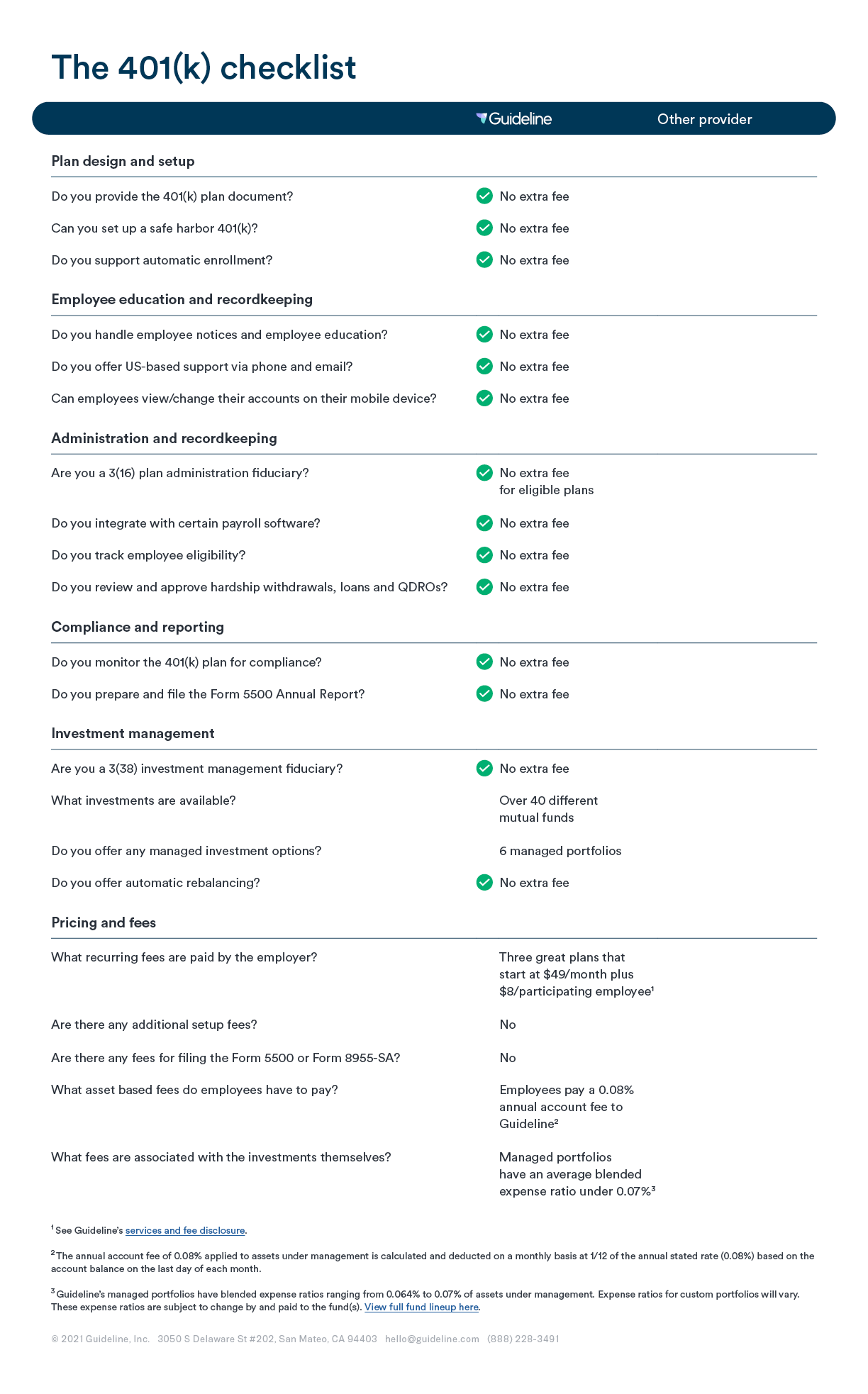

As the saying goes, “you don’t know what you don’t know.” When you’re on the phone, knowing what to ask for is half the battle. Download our free, one-page 401(k) Vendor Checklist and learn exactly what to look for.

We’ll list the features you should look for and the questions you need to ask. As you evaluate vendors, see if they check all the boxes — and how their offerings compare to ours.

{kind=link}