IRA 101: What they are and how they can help you save for retirement

An IRA, or individual retirement account, is a tax-advantaged investment account designed to help you reach your retirement goals. Whether you’re just starting your career or getting close to retirement, an IRA can help you build a strong financial foundation for the future. In this post, we’ll cover:

- How an IRA can help you reach your retirement goals

- The different types of IRAs

- How much you can save with an IRA

What is an IRA?

IRA stands for Individual Retirement Account. These accounts are tax-advantaged, which means they have tax benefits.

Unlike a 401(k), IRA’s aren’t linked to an employer. That means you can open an IRA independently whenever you want, even if you do or don't have a company-sponsored 401(k).

There are two types of personal IRAs:

- With a traditional IRA, your contributions are pre-tax, just like a 401(k). Your invested funds will be tax-deferred, which means you pay taxes when you withdraw money at retirement.

- In a Roth IRA, your contributions are after-tax and investments grow tax-free. Your qualified withdrawals in retirement are tax-free.¹

And there’s the rollover IRA — more to come on that below.

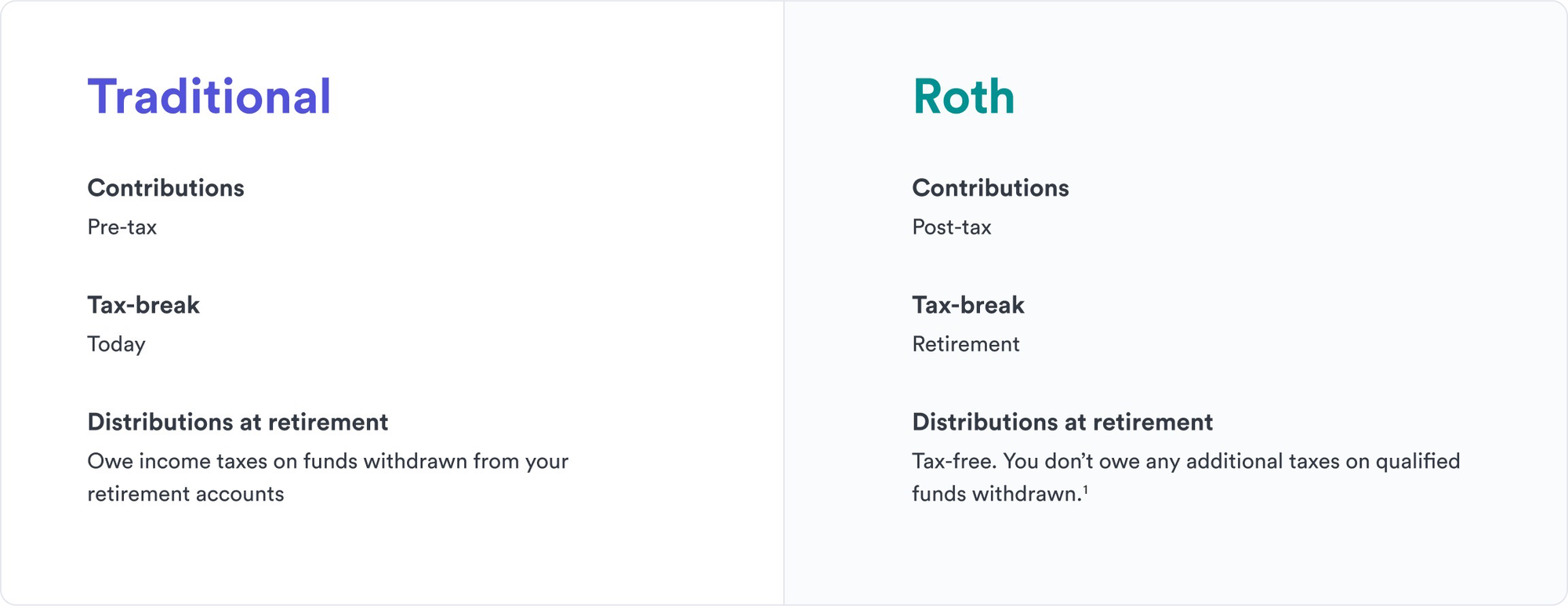

What is the difference between a traditional and Roth IRA?

The key difference between traditional and Roth retirement accounts is when you receive a tax break. An easy way to remember this is:

- Traditional = today

- Roth = retirement

With a traditional IRA, you get the tax advantage today. This is because you can claim your contribution as a deduction to your taxable income for that year. For example if your taxable income is $60,000 for the year, and you contributed $5,000 to your traditional IRA, your taxable income drops down to $55,000. When you request a distribution, which is money you want to withdraw, in retirement, it will be taxed as income. There is no distinction between what you contributed and what you earned by being invested; the entire withdrawal counts as income.

With a Roth IRA, you can enjoy the tax advantage at the time of retirement. Your contributions are after-tax and therefore cannot be claimed as a deduction to your income in the year you make the contribution. Using the same example as above, if your taxable income is $60,000, and you contribute $5,000 to a Roth IRA, your taxable income for that year is still $60,000. That being said, anything that is distributed in retirement is tax-free. Because of the after-tax status of Roth IRAs, the IRS has income limits that determine whether or not you may contribute.

What are the benefits of an IRA?

IRAs are a retirement option for anyone who earns taxable income in a given tax year. They’re a great way for savers to reach their retirement goals, whether you’re self-employed or want to save outside of your employer-sponsored 401(k).

Tax-advantaged

For starters, your contribution to an IRA may lower your taxable income, which is how much of your income is subject to state and federal income taxes. Additionally, as your balance fluctuates alongside the market, you will not be subject to capital gains taxes like you would in taxable investment accounts. This is why the IRS limits how much an individual may contribute each year.

More flexibility

In addition to the tax benefits, IRAs offer more flexibility compared to a 401(k). For example, the IRS allows early withdrawals up to $10,000 without penalty for first time home buyers.

More autonomy and options

Also, with a 401(k), you are a participant in your company’s plan. They can change the plan or the plan’s investments at any time and they don’t need your approval to make those changes. Plus, if you leave that job, you lose the ability to contribute to that 401(k). But with an IRA, the account is yours to manage as you see fit. Also, IRAs tend to offer more investment options than 401(k)s, allowing you control of how you want to invest your money, such as stocks, bonds, and mutual funds.

Who should consider an IRA?

An IRA can help anyone reach their long-term savings goals no matter where they are in their retirement journey. An IRA may be a fit for individuals who:

- Want to start saving for retirement now

- Have one or more 401(k)s or other retirement accounts from previous employers and are interested in consolidating their savings

- Already have an employer-sponsored 401(k) and are interested in saving additional funds for retirement

As with any financial decision, consult an advisor or tax professional to help determine if an IRA could be a retirement savings option for you.

What is a rollover IRA?

Now onto the rollover IRA. Many savers open an IRA to “roll over” funds from existing retirement accounts like a 401(k), 403(b), or 457(b) from a previous employer. It might seem like a "rollover IRA" is its own category, but in reality, it’s just a traditional IRA or Roth IRA with the same tax advantages and contribution limits. Which type of IRA you choose to "roll over" your funds into is entirely up to you.

Rollover IRAs make sense for savers looking to consolidate several retirement accounts. Doing so can help you keep track of your savings goals and potentially save you money by reducing or eliminating fees or commissions charged on each account.

How much can I contribute to an IRA?

You can make contributions to your IRA as long as you have taxable income in a given tax year. In 2023, individuals can contribute $6,500 to their traditional or Roth IRA. Individuals 50 and older can make an additional catch-up contribution of $1,000.

Two important things to note here:

- Contributions to all of your IRA accounts combined cannot exceed the IRS’ annual limit, which is $6,500 in 2023. (For example, you can’t contribute $6,000 to a Roth IRA with Guideline and another $2,000 with another institution.)

- Only new deposits count as a contribution. If you are consolidating accounts and simply rolling money over to an IRA, that does not count as a contribution.

Can I have a 401(k) and an IRA?

Yes. It’s a common misconception that you can only have a 401(k) or an IRA, but you can have and contribute to both.

How much does an IRA cost?

Like a 401(k), an IRA typically has account management fees, which are a percentage of the value of your portfolio. When choosing an IRA, it’s a good idea to understand and compare account management fees across different account providers, as those fees can add up. You’ll also need to consider the expense ratios, which are the cost of the investments themselves.

At Guideline, we’ve made it our mission to help everyone arrive at a secure retirement, which is why we’ve designed an IRA that is:

- Affordable: Accounts start at $2 per month plus an 0.08% annual account fee, which is equivalent to 67¢ for every $10,000 saved.²

- Easy: Get started with our investment questionnaire and keep your savings in check with automatic rebalancing of your portfolio.

- Flexible: Choose from one of our managed portfolios or build a custom portfolio using our selected low-cost funds.

Finding your road to retirement

It’s never too early or too late to save for your future. Learn more about setting up an IRA with us. And if you found this content helpful, here are a few more resources you might be interested in:

- Curious how much you can save for retirement this year? Good news: contribution limits are up for 2023.

- Compound interest can have a big impact on your retirement savings — here’s how.

- Are you self-employed? Setting up a SEP IRA is a low-stress, flexible way to help you and your employees plan for retirement.

This information is general in nature and is for informational purposes only. It should not be used as a substitute for specific tax, legal and/or financial advice that considers all relevant facts and circumstances. You’re advised to consult a qualified financial adviser or tax professional before relying on this information.

¹ Roth distributions will be tax-free if the following conditions are met: (a) you're over age 59 1/2 AND (b) it has been 5 years since your first deposit.

² This information is for illustrative purposes only, and is not intended to be construed as investment or tax advice. Information shown here assumes a static balance of $10,000 per month, an annual account fee of 0.08% on assets under management (calculated and deducted on a monthly basis at 1/12 of the annual stated rate (0.08%) based on the month-end account balance) and does not account for common factors that affect the value of your account balance over time such as gains, losses, distributions, additional contributions, etc. It’s not intended to be taken as investment advice or as an assurance or guarantee of future performance. The fee presented does not include other fees that an IRA owner may incur, including, but not limited to, from mutual fund expense ratios.